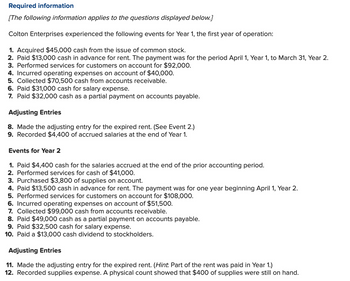

In accordance with the average of all the almost every other banking companies, Basic Republic got good proclivity so you can run scorching which have regular mortgage-to-deposit percentages about higher 80’s to even more than 100%. This is exactly a hostile approach to lending you to seeks to maximize produce while you are losing exchangeability. The latest willful decision to operate at that higher mortgage-to-deposit ratio pleased people having higher returns on the assets however, did maybe not get-off far place to own mistake. Because Buffet has said, If tide is out, we come across that is diving naked. That’s just what i spotted if the illiquidity of one’s mortgage portfolio is along side historical distributions from dumps.

Running to the exits

In the event the interest hikes had pulled complete impression of the stop out-of 2022, of numerous people and you can lender people expanded smart to the new facts that has been haunting financial harmony sheet sets. Longer-duration property for example >30-time Valuable Bonds and you may Mortgages which have been originated a vastly lower interest ecosystem, subjected banking institutions to tall liquidity dangers on account of a beneficial mismatch in the new readiness of one’s assets (securities, mortgages) and you can liabilities (deposits). Many of these banks had been mostly funded of the consult dumps, money-places and you may quick-identity Cds. So you’re able to aggravate the issue, 68% off Earliest Republic’s complete deposits was basically beyond the $250,000 number of FDIC deposit insurance rates. Which have customers smell something fishy and being fearful off losing the uninsured places, of many started to withdraw dumps off Very first Republic.

Since seen in it chart (right), a rush more than $70B off deposits occurred in Q1’2023. It run using the lending company is historical and you may try 50x any exchangeability demand the financial institution had observed in for the last according to the fresh trust of the Advantage Accountability Panel (ALCO) so you can have confidence in an effective $step one.5B borrowing business on Government Home loan Lender. The bank survived Q1’2023 and stayed to battle a different sort of one-fourth thanks a lot to your surge regarding $30B for the places provided with a great consortium out-of eleven finance companies led of the JPMorgan, Citigroup and Wells Fargo in the middle of March.

Real time to fight another type of one-fourth

Additional borrowings out of First Republic increased when faced with deposit withdrawals and you can an illiquid loan collection generally composed of mortgage loans. First Republic went to new Government financial Lender so you can use $35B and lent $77.3B off their offer including the consortium off banking companies referenced in the past. The majority of these borrowings happened later in the 1st one-fourth as can get noticed because of the mediocre stability out-of Most other Borrowings said for your quarter have been simply $37.5B. We will keep in mind that the fresh $35B out of borrowings on Government Home loan Lender are a far cry on $1.5B personal line of credit stated regarding SEC ten-Q processing from Q3’2022. Just how one thing changes in half a year!

It wasn’t bonds determined

Once the illiquidity motivated from the financial portfolio is the protagonist of the facts, there have been as well as a great deal of to 2022. Much less for the magnitude versus financial portfolio, the latest ties collection wasn’t an element of the adding foundation on the inability out of Earliest Republic. That it ties collection try primarily including brief-cycle (

Shed profits

While making things worse, while the bank try facing an exchangeability crisis, the earnings was also are squeezed. With enough time-dated repaired-price assets which were not lso are-pricing anytime soon along side a deposit base regarding better-knowledgeable users seeking produce to the both demand and go out dumps, the financial institution watched small grows when you look at the notice earnings out-of the loan origination and therefore did not been near to offsetting brand new remarkable expands inside appeal expenses in this “” new world “” best personal loans bad credit Arkansas interesting price nature hikes.