According to 5 U.S.C. 553(b)(4), a listing of it proposed laws can be discover of the heading so you’re able to along with the latest Search for dockets and data into the department measures box, enter the following docket matter RHS-24-SFH-0029.

Laurie Mohr, Fund and you can Mortgage Analyst, Single Friends Homes Protected Mortgage Section, Rural Development, You.S. Agency out-of Agriculture, Avoid 0784, Area 2250, Southern area Agriculture Strengthening, 1400 Independence Avenue SW, Washington, DC 20250-0784. Telephone: (314) 679-6917; or email address:

I. Statutory Expert

SFHGLP is authorized at the Section 502(h) regarding Label V of your Property Work out-of 1949 (42 You.S.C. 1472(h)) and you will used because of the seven CFR region 3555.

II. Records

RHS also offers multiple applications to create or improve homes and essential society establishment within the outlying parts. RHS now offers fund, gives, and you will financing promises for single and you may multi-loved ones housing, childcare centers, fire and you will cops programs, hospitals, libraries, assisted living facilities, colleges, basic responder automobile and you may gadgets, casing to own ranch laborers plus. RHS now offers technology guidance loans and has in partnership with non-cash groups, Indian tribes, Federal and state Regulators providers, and you may local teams.

Under the authority of one’s Casing Work out-of 1949, (42 U.S.C. 1471 et seq.), as the amended, new SFHGLP tends to make financing guarantees to add lowest- and you can average-income individuals inside the rural elements the opportunity to individual pretty good, safer, and you will hygienic dwellings and you can related establishment. Accepted loan providers make initial qualification determinations, plus the Department evaluations those people determinations and also make a final qualification choice.

This method support lenders work with lowest- and you may average-money properties staying in rural portion and also make homeownership a real possibility. Providing affordable homeownership opportunities promotes success, which creates thriving organizations and you may improves the top-notch lives for the rural parts.

III. Conversation of Advised Code

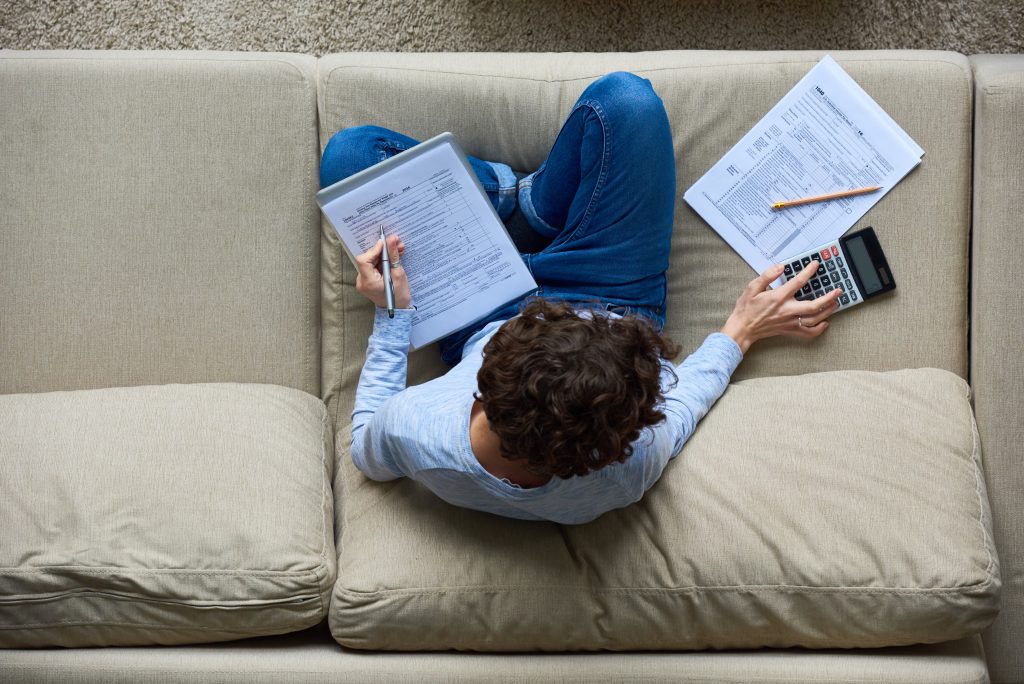

Currently, a candidate that have an indication of tall derogatory borrowing from the bank needs an effective bank to conduct then feedback and document that feedback during the new underwriting procedure. Since specified in 7 CFR 3555,151(i)(3)(iv), that sign out-of tall derogatory borrowing are a past Institution financing made to new candidate one triggered a loss towards the Bodies. A loss allege on the a beneficial SFHGLP or a single Family relations Homes Lead Loan contributes to a loss of profits into authorities. For this reason, an applicant having an earlier losses claim is to own an indication off significant derogatory borrowing from the bank.

Candidates obtaining a promise from the SFHGLP must obtain a very clear Credit Aware Verification Reporting System (CAIVRS) matter, and this checks to have earlier losings claims of the reviewing one unpaid and you can/otherwise defaulted claims that were repaid on the applicant’s account. Currently, long lasting go out introduced given that a loss into the ( printing webpage 76746) Institution taken place, applicants need certainly to care for a clear CAIVRS number to find a different sort of financing into SFHGLP.

So it proposed laws intends to amend https://availableloan.net/loans/short-term/ eight CFR (i)(3)(iv) to establish a period of time maximum for how a lot of time an earlier Department losses would be sensed extreme derogatory borrowing from the bank. The fresh Institution reveals that the time limit become eight age. This would imply that any losses declare that are more than 7 yrs old do no longer be considered extreme derogatory credit having a candidate obtaining a different sort of loan utilising the SFHGLP.

It proposed laws perform greatest fall into line new prepared period having those used by equivalent programs. Brand new Pros Management (VA) in addition to Government Housing Administration (FHA), part of the You.S. Agency from Housing and Metropolitan Innovation, keeps shorter wishing symptoms prior to people meet the requirements to sign up its home loan software immediately following having a property foreclosure. Va allows people to try to get a mortgage since 2 years shortly after a past foreclosures, having FHA with a great about three-seasons prepared months. While a previous losings claim is a significant experiences whether or not it happen, applicants will create confident payment feature throughout the years as a result of various function, such building credit; getting top purchasing work; exhibiting growth of liquid assets; and you may location by themselves is qualified to receive homeownership from the SFHGLP. Already, 7 CFR (i)(3) makes it necessary that for yourself underwritten funds, lenders need certainly to fill out paperwork of your own borrowing from the bank degree decision. Loan providers explore credit scores so you’re able to by hand underwrite mortgage home loan requests and are required to confirm the financing score found in the newest underwriting commitment. Indications away from significant derogatory borrowing from the bank require then remark and you can paperwork away from you to definitely review and you can a past Company loan you to definitely resulted in a loss on the regulators is certainly one item that would want which brand of significantly more comprehensive underwriting opinion and you may files.